TODO SUMMARISE MONITORING AND CONTROLLING ⏫ 📅 2024-02-28

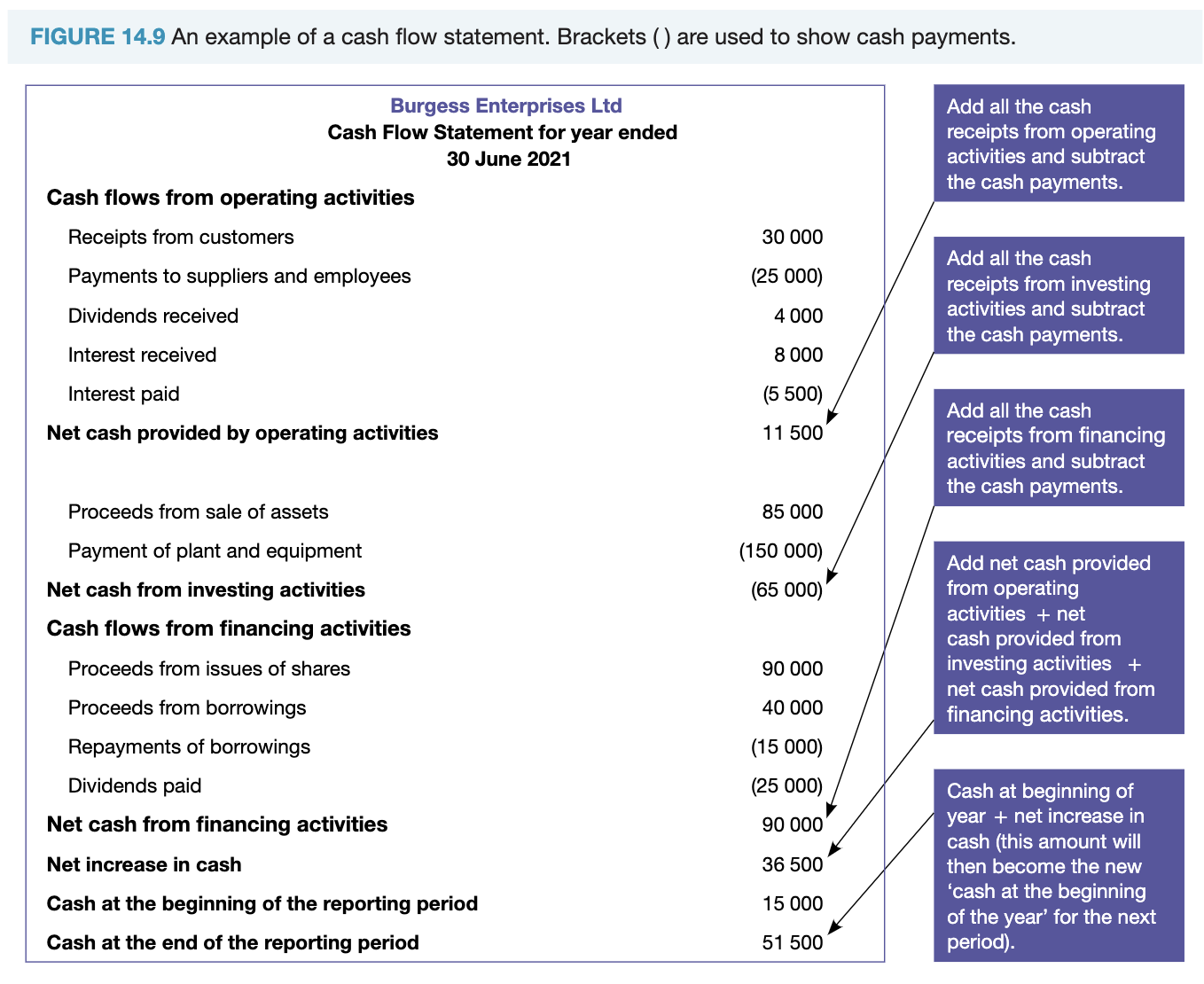

Cash flow statements

a Cash flow statement is :: a financial statement that indicates the movement of cash receipts and cash payments resulting from financial transactions over a period of time

The cash flow statement is further broken down into:

?

Operating activities: cash inflows and outflows relating to the business’ main activity

Investing activities: cash inflows and outflows relating to the purchase and sale of non-current assets and investments

Financing investments: cash inflows and outflows relating to the business’ borrowing activities

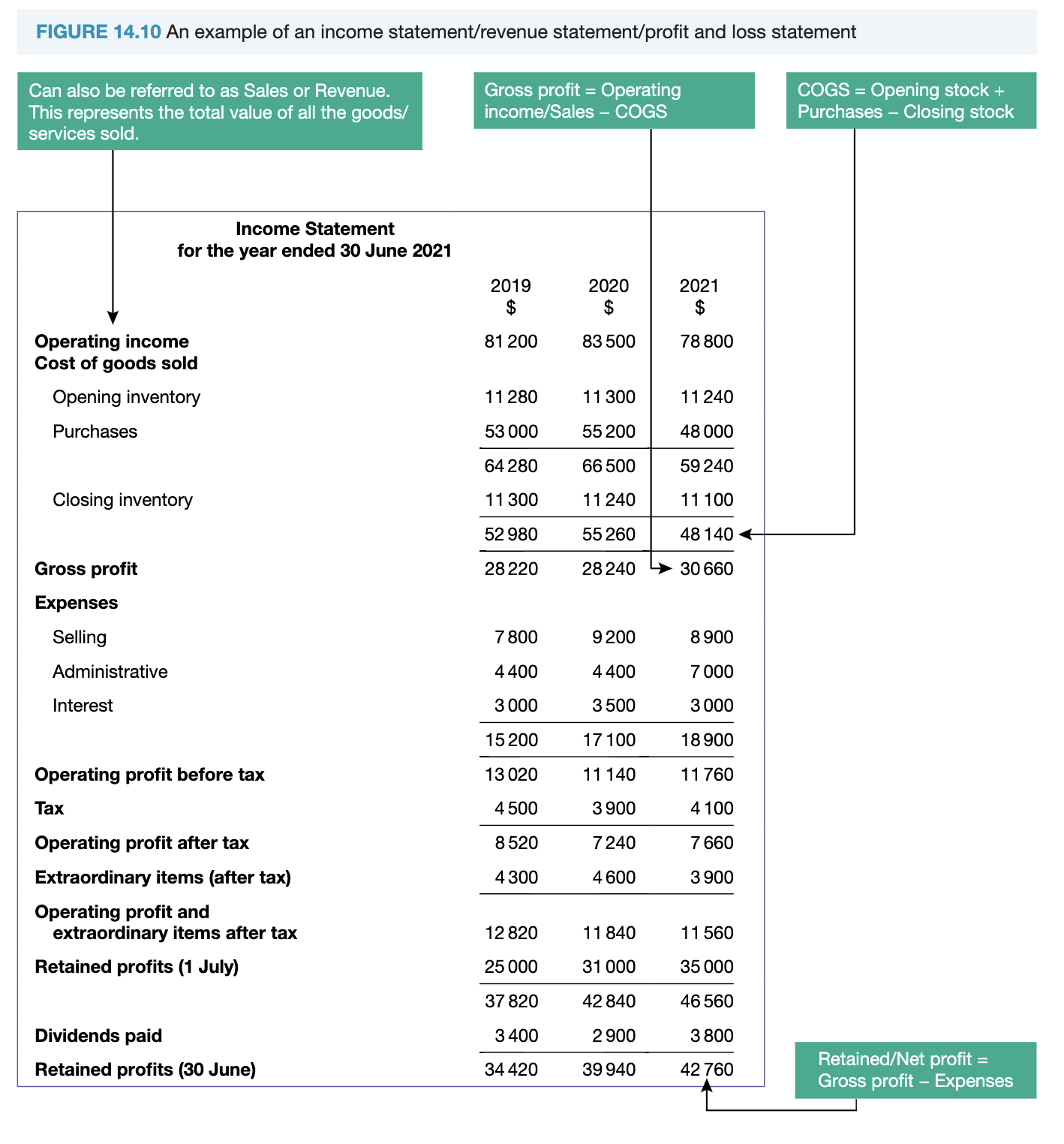

Income statements

The income statement(a.k.a. revenue/profit & loss statement) is :: a summary of the income earned and the expenses incurred over a period of trading.

assists in assessing:

how the money has come into the business,

how much has gone out as expenses,

how much has been derived as profit.

The following formulas are required for the income statement:

COGS = opening stock + purchases – closing stock

cost of goods sold (COGS) is :: the value of stock that a business has sold to its customers (what it cost to make what they have sold)

Gross profit = sales – COGS

gross profit is :: that part of a business’s profit that represents operating income minus cost of goods sold (sales - COGS)

Net profit = gross profit – expenses

net profit the difference between the gross profit and expenses (includes all expenses, not just the COGS)

example:

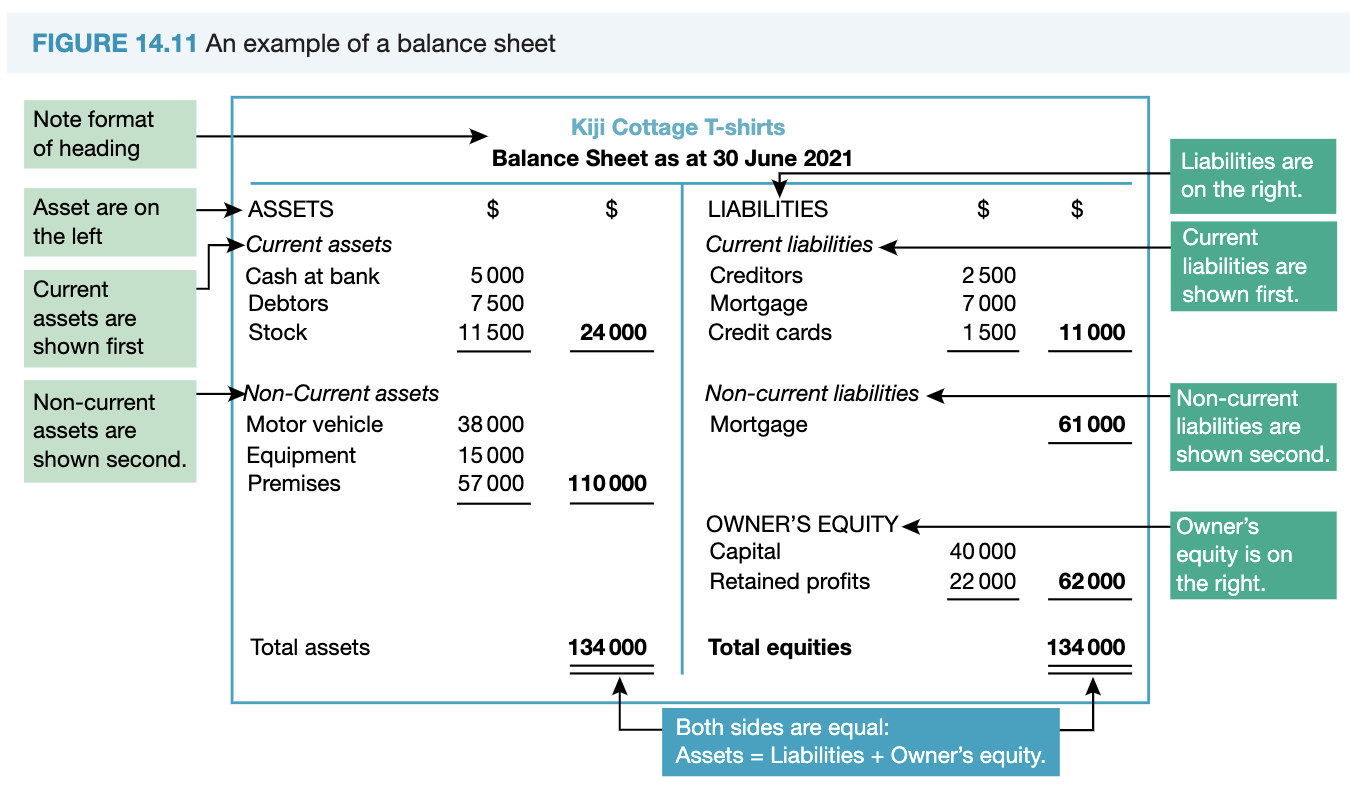

Balance sheets

a Balance sheet represents :: a business’ assets and liabilities at a particular point in time and represents the net worth of the business.

Assets are :: items of value owned by a business

- Current assets - can expect to use up, or turn over, within 12 months

- Non-current assets - have an expected life of longer than 12 months

liabilities are :: items of debt owed to outside parties

- Current liabilities - debts which are expected to be repaid in less than 12 months

- Non-current liabilities — long-term items of debt

owners’ equity is :: the funds contributed by the owner(s); represents the net worth of the business

example:

mortgage is never current?

the accounting equation and relationships

The Accounting equation shows

?

the relationship between assets, liabilities, and owner’s equity