-

TODO limitations of financial reports notes 📅 2024-03-08

-

Limitations refer to the shortcomings of accuracy in disclosed financial reports

- each limitation are opportunities for ambiguity

- to which businesses can present their financial situation as better off

Normalised earnings

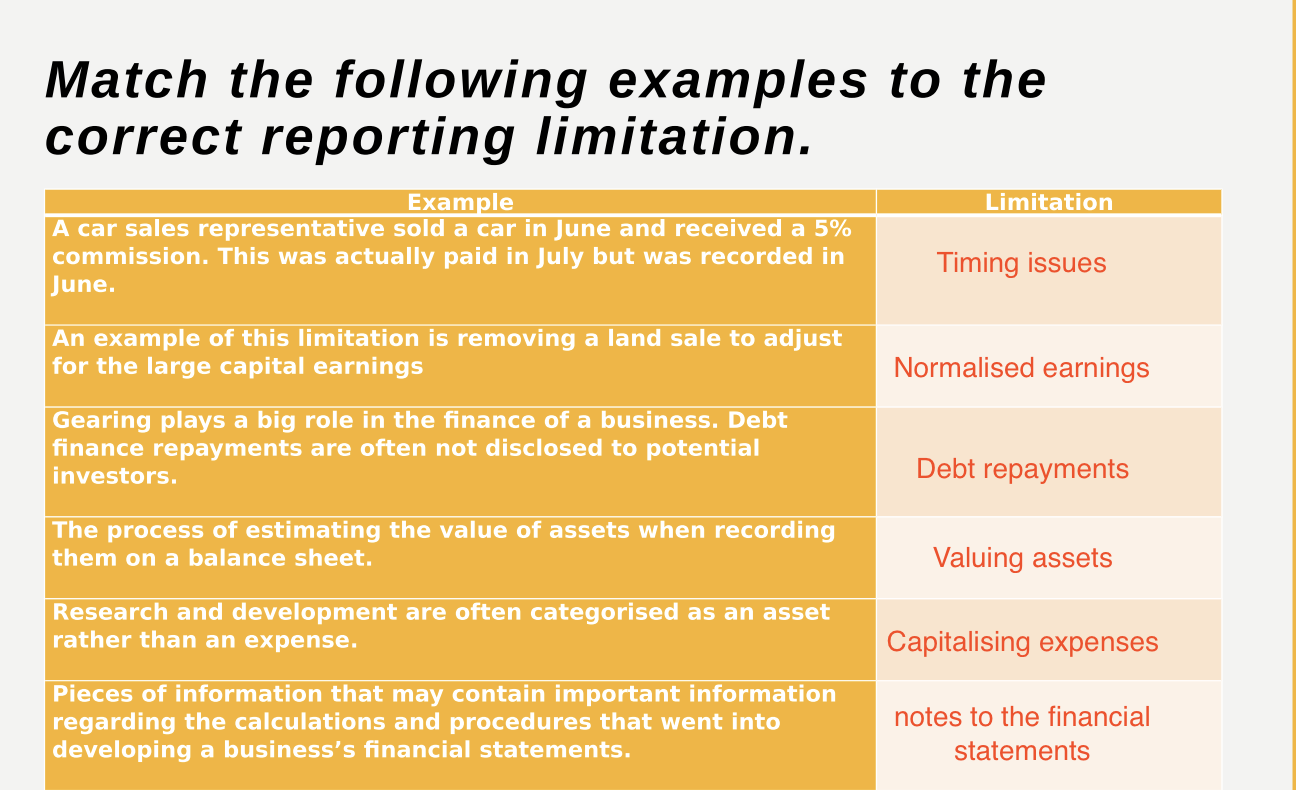

- Normalised earnings are :: the earnings that have been adjusted to take into account changes in the economic cycle or to remove one-off items that may distort profitability such as the sale of land.

- makes it easier to compare profitability figures from different years and against other businesses.

Capitalising expenses

- Capitalising expenses is :: an accounting method where a business records an expense as an asset on the balance sheet rather than an expense on the income statement.

- where expenses are regarded as a capital item and put into the balance sheet rather than the P&L

- e.g. a business spends $30m on Research and development

- which produces a patent valued at $25m

- hence the $25m patent is placed on the balance sheet as an asset

- and the -$5m difference (loss) is recorded on the income statement. (where it originally belongs)

Valuing assets

?

- Valuing assets is : the process of estimating the value of assets when recording them on a balance sheet.

- Valuing assets can be difficult, the asset may be recorded at its historical cost

- where assets are listed with their value at the time of purchase

- additionally it can be difficult to value intangible assets, such as:

- goodwill

- trademarks

- patents

- brand names

Timing issues

- The matching principle is a fundamental accounting concept

- The matching principle states

? - that expenses incurred by a business must be recorded on the income statement for the accounting period in which the revenue is earned.

- (i.e. the costs associated with generating revenue from a certain source should be reported adjacent to the said revenue to give a more accurate picture)

- even if the costs were a financial period before

- (i.e. the costs associated with generating revenue from a certain source should be reported adjacent to the said revenue to give a more accurate picture)

- e.g. a house is sold (in June), but the money is not paid until months later (August)

- The expense should be recorded in June

Debt repayments

?

- Debt repayments refers to : either the money owed to the business or by the business.

- The gearing ratio determines whether a business is at risk of meeting long-term financial obligations.

- fluctuations in gearing affect risk and potential profits

- financial reports are limited as they do not have the capacity to disclose specific information about debt repayments.

- sometimes debt repayments can be used to distort the reality of the businesses financial status

Notes to the financial statements

?

- The notes to the financial statements include any additional information that is left out of the main financial reporting statements.

- contains info useful to stakeholders to make sense of financial statements, for example, extra info on;

- the accounting methodologies,

- inventory valuation techniques